All Categories

Featured

Table of Contents

Seek advice from your family members and financial team to figure out if you are wanting to obtain payouts immediately. If you are, a prompt annuity might be the most effective option. No issue what option you select, annuities help provide you and your family members with economic protection. As with any kind of monetary and retired life decisions, talking to monetary experts before making any decisions is advised.

Warranties, consisting of optional benefits, are backed by the claims-paying ability of the company, and might have limitations, consisting of surrender costs, which might affect plan worths. Annuities are not FDIC guaranteed and it is feasible to lose money. Annuities are insurance coverage items that need a premium to be spent for purchase.

Please contact an Investment Expert or the releasing Firm to get the syllabus. Capitalists need to take into consideration financial investment purposes, risk, charges, and expenditures thoroughly before investing.

Annuity Guys Ltd. and Client One Stocks, LLC are not affiliated.

The warranties use to: Settlements made built up at the interest rates applied. The cash money worth minus any type of fees for paying in the policy.

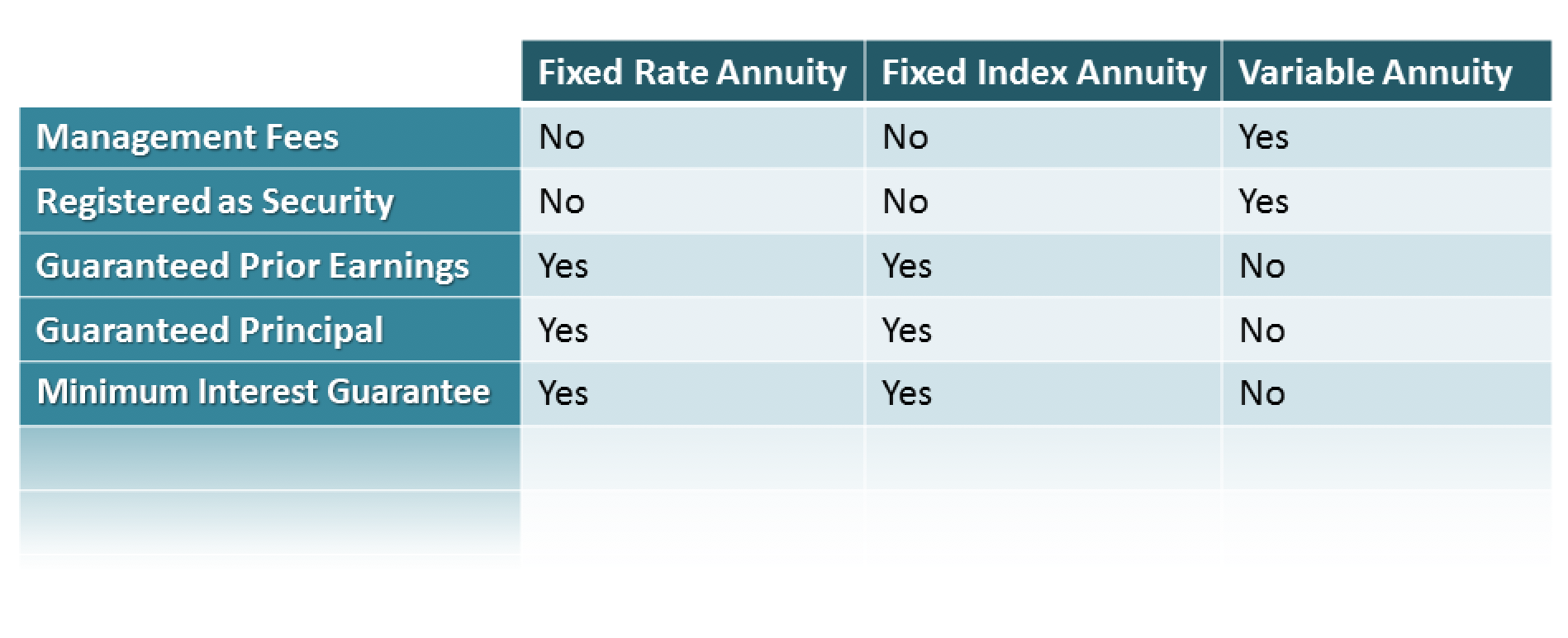

The price put on the cash worth. Repaired annuity rates of interest provided adjustment consistently. Some taken care of annuities are called indexed. Fixed-indexed annuities use development capacity without securities market risk. Index accounts credit scores some of the gains of a market index like the S&P 500 and none of the losses. The values of a variable annuity are financial investments picked by the proprietor, called subaccount funds.

Decoding How Investment Plans Work Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Variable Annuity Vs Fixed Annuity Why Choosing the Right Financial Strategy Is a Smart Choice Fixed Index Annuity Vs Variable Annuities: How It Works Key Differences Between Tax Benefits Of Fixed Vs Variable Annuities Understanding the Risks of Variable Annuities Vs Fixed Annuities Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Immediate Fixed Annuity Vs Variable Annuity A Closer Look at Fixed Vs Variable Annuities

They aren't assured. Money can be moved in between subaccount funds without any kind of tax repercussions. Variable annuities have actually features called living advantages that supply "drawback protection" to investors. Some variable annuities are called indexed. Variable-indexed annuities offer a level of defense versus market losses picked by the financier. 10% and 20% downside defenses are typical.

Dealt with and fixed-indexed annuities frequently have during the surrender period. The insurance policy company pays a set price of return and absorbs any market danger.

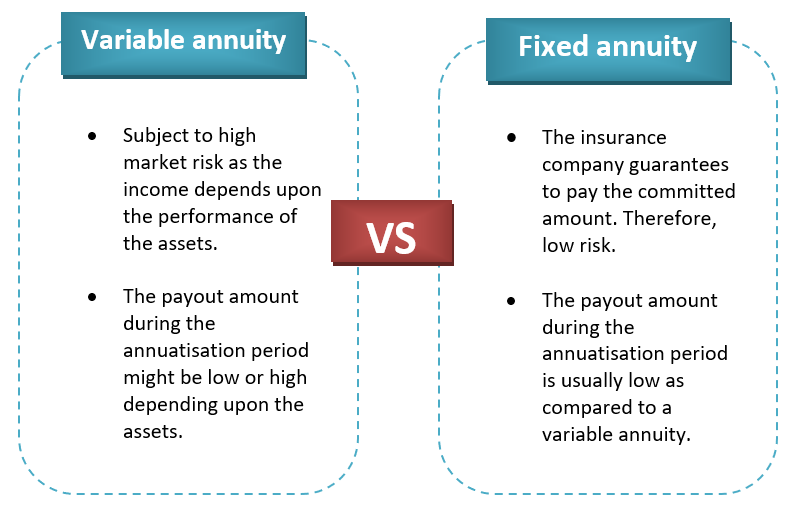

Variable annuities also have earnings alternatives that have actually assured minimums. Some capitalists make use of variable income as a tool to keep up with rising cost of living in the future. Others choose the assurances of a fixed annuity earnings. Fixed annuities use warranties of principal and rates of return. Variable annuities offer the potential for greater development, together with the danger of loss of principal.

Highlighting Fixed Vs Variable Annuity Pros And Cons Everything You Need to Know About Financial Strategies Defining the Right Financial Strategy Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Is Worth Considering Retirement Income Fixed Vs Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Risks of Annuities Fixed Vs Variable Who Should Consider Fixed Interest Annuity Vs Variable Investment Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Fixed Vs Variable Annuity Pros Cons Financial Planning Simplified: Understanding Pros And Cons Of Fixed Annuity And Variable Annuity A Beginner’s Guide to Deferred Annuity Vs Variable Annuity A Closer Look at Variable Vs Fixed Annuity

Variable annuities have several optional benefits, however they come at a price. The expenses of a variable annuity and all of the choices can be as high as 4% or more.

Insurer using indexed annuities offer to shield principal in exchange for a limitation on growth. Fixed-indexed annuities assure principal. The account worth is never ever much less than the initial acquisition settlement. It is essential to remember that surrender charges and various other charges may apply in the very early years of the annuity.

The growth possibility of a fixed-indexed annuity is typically much less than a variable indexed annuity. Variable-indexed annuities do not assure the principal. Instead, the financier picks a degree of downside protection. The insurer will certainly cover losses approximately the level selected by the capitalist. The growth potential of a variable-indexed annuity is usually greater than a fixed-indexed annuity, but there is still some threat of market losses.

They are well-suited to be a supplemental retired life cost savings strategy. Here are some points to think about: If you are adding the maximum to your office retired life plan or you don't have access to one, an annuity may be a good option for you. If you are nearing retired life and need to produce guaranteed income, annuities provide a variety of alternatives.

If you are an active investor, the tax-deferral and tax-free transfer features of variable annuities may be eye-catching. Annuities can be an important part of your retired life strategy.

Breaking Down Your Investment Choices Everything You Need to Know About Financial Strategies Breaking Down the Basics of Variable Vs Fixed Annuity Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Is a Smart Choice Fixed Income Annuity Vs Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Key Features of Long-Term Investments Who Should Consider Fixed Annuity Vs Equity-linked Variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Variable Annuities Vs Fixed Annuities A Beginner’s Guide to Fixed Vs Variable Annuities A Closer Look at Deferred Annuity Vs Variable Annuity

Any details you offer will only be sent out to the representative you pick. Resources Advisor's guide to annuities John Olsen NAIC Customers direct to delayed annuities SEC guide to variable annuities FINRA Your Overview To Annuities- Variable Annuities Fitch Ratings Definitions Moody's rating scale and meaning S&P International Understanding Scores A.M.

Best Economic Score Is Vital The American College of Count On and Estate Guidance State Survey of Possession Protection Techniques.

An annuity is an investment option that is backed by an insurance policy firm and provides a series of future payments in exchange for present-day deposits. Annuities can be extremely personalized, with variations in rate of interest, costs, taxes and payouts. When choosing an annuity, consider your special demands, such as for how long you have prior to retired life, just how rapidly you'll need to access your cash and how much tolerance you have for threat.

Breaking Down Your Investment Choices Everything You Need to Know About Variable Vs Fixed Annuity Defining Pros And Cons Of Fixed Annuity And Variable Annuity Benefits of Immediate Fixed Annuity Vs Variable Annuity Why Fixed Income Annuity Vs Variable Annuity Matters for Retirement Planning How to Compare Different Investment Plans: A Complete Overview Key Differences Between Annuities Variable Vs Fixed Understanding the Rewards of Variable Annuities Vs Fixed Annuities Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Fixed Income Annuity Vs Variable Growth Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Variable Annuity Vs Fixed Annuity

There are several sorts of annuities to pick from, each with special attributes, threats and incentives. Thinking about an annuity? Right here's some things to take into consideration regarding the different kinds of annuities, so you can attempt to select the very best option for you. An annuity is a financial investment alternative that is backed by an insurance policy business and supplies a series of future payments in exchange for contemporary deposits.

Your payments are made during a duration called the build-up stage. Once spent, your cash expands on a tax-deferred basis. All annuities are tax-deferred, implying your interest earns interest up until you make a withdrawal. When it comes time to withdraw your funds, you may owe taxes on either the complete withdrawal quantity or any kind of interest built up, relying on the kind of annuity you have.

During this time, the insurance firm holding the annuity disperses routine settlements to you. Annuities are used by insurance firms, financial institutions and various other monetary establishments.

Set annuities are not attached to the variations of the securities market. Instead, they expand at a set interest rate identified by the insurance firm. Consequently, repaired annuities are considered one of one of the most dependable annuity choices. With a taken care of annuity, you might receive your repayments for a collection period of years or as a swelling sum, relying on your contract.

With a variable annuity, you'll pick where your payments are invested you'll typically have low-, moderate- and high-risk options. Consequently, your payments enhance or reduce in connection with the efficiency of your picked portfolio. You'll receive smaller payments if your financial investment chokes up and bigger payments if it executes well.

With these annuities, your contributions are connected to the returns of one or even more market indexes. Lots of indexed annuities also include an ensured minimum payment, similar to a fixed annuity. In exchange for this extra protection, indexed annuities have a cap on just how much your investment can gain, also if your selected index does well.

Understanding Financial Strategies Key Insights on Fixed Vs Variable Annuities What Is the Best Retirement Option? Advantages and Disadvantages of Fixed Annuity Vs Variable Annuity Why Fixed Vs Variable Annuities Matters for Retirement Planning How to Compare Different Investment Plans: A Complete Overview Key Differences Between Fixed Index Annuity Vs Variable Annuities Understanding the Key Features of Fixed Vs Variable Annuity Who Should Consider Choosing Between Fixed Annuity And Variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Vs Variable Annuity Pros Cons A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Vs Variable Annuities

Below are some benefits and drawbacks of various annuities: The main benefit of a taken care of annuity is its predictable stream of future earnings. That's why fixed-rate annuities are usually the go-to for those preparing for retirement. On the other hand, a variable annuity is much less foreseeable, so you will not get an ensured minimum payment and if you select a high-risk investment, you could even shed money.

Yet unlike a single-premium annuity, you usually won't be able to access your payments for several years to find. Immediate annuities provide the choice to obtain revenue within a year or more of your financial investment. This may be a benefit for those dealing with brewing retired life. Nevertheless, funding them commonly needs a large amount of money in advance.

{kind=link}

Latest Posts

American General Annuity Withdrawal Form

Today's Best Multi-year Guaranteed Annuities (Mygas)

F&g Annuities And Life Mailing Address